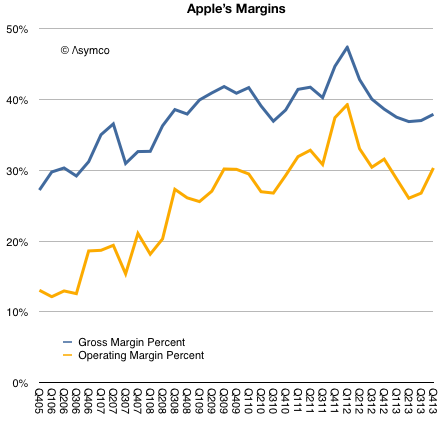

Prior to Apple’s earnings report I read at least one article suggesting that the most important indicator to watch was Apple’s margin. I suppose this was due to a recent decline in margins from a peak gross margin of 47.4% in Q1 2012 to 36.7%.

As the graph below shows, margins began to recover by Q3 2013 and are nearly on par with year-ago levels.

The guidance for the present quarter is a gross margin between 37% and 38%. This would imply a flat q/q GM line (blue line above.)

This is not quite catastrophic.

To better understand margins, it helps to compare them with other companies. When Apple reached that peak of near 50% gross margin I noted that such a level was higher than Microsoft’s and Google’s. The irony being that Apple was nominally an (implied) low-margin hardware company while Microsoft was an (implied) high-margin software company and Google was an (implied) high-margin internet services company.

Here is the picture with the last two years added: Continue reading “A margin of error”