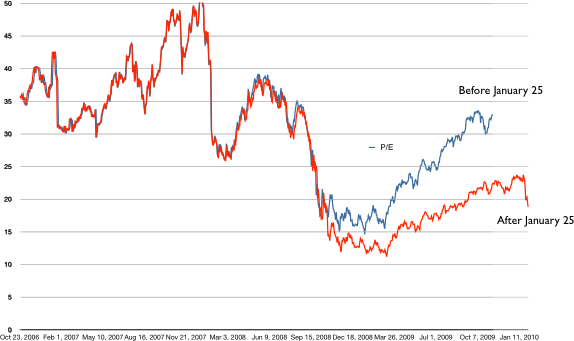

Apple trading below 20 P/E (18.9 today vs. 33 pre-re-statement)

Apple trading below 20 P/E (18.9 today vs. 33 pre-re-statement)

It had dropped to 11 in early 2009.

Apple trading below 20 P/E (18.9 today vs. 33 pre-re-statement)

It had dropped to 11 in early 2009.

It’s time to re-evaluate the categorization of smartphones. The term has always been problematic. It loosely means a phone that runs an advanced operating system and has third party SDKs. There is no industry standard definition and some call it a converged device or a multimedia device. One analyst famously said that the iPhone did not count as a smartphone on launch because it was not open to developers.

I’d propose a different definition, not based on the attributes of the device, but the jobs that the device is hired to do. This is in a way, the same distinction between Facebook and MySpace. They are clearly hired to do different things by their users and as a result don’t directly compete. When you do this job-based segmentation, you realize that iPhones, Android devices and Windows Mobile and Palm are fairly similarly used. Blackberry, however, does not match the profile. (Neither do most recent Symbian devices, though for different reasons.)

The most common jobs I can see in use with the first cohort of devices is (Comscore data exists to back this up)

The Blackberry has relatively poor utilization of any function except for email and perhaps social networking (though the latter is not likely in company-sourced devices). The focus on a large number of jobs to be done is what distinguishes smartphones from the more limited “feature phones”. By this logic Blackberry is hired as a “feature phone”.

It’s also instructive to follow commentary among enthusiasts. It’s fairly clear that this segmentation exists implicitly: Android, iPhone, Palm and WinMo are comparable while Blackberries are for a different demographic, different user, different usage.

Finally, there is the gut check. It’s become clear to me that what users do with Blackberries is similar to what they do with voice phones: voice and messaging. Although additional functionality is available, it hardly gets used because it’s hard to use.

But you may ask: so what? The reason this is significant is that smartphones are embryonic mobile computers with a clear trajectory for improvement. Feature phones are overshot voice phones which are likely to be disrupted by data-centric entrants.

On a different level, it also means that growth stats for the two product types are not comparable. Saying that the Blackberry is outgrowing the iPhone (or vice versa) is meaningless.

It also means that Blackberries, being an evolution of voice products, still have a huge growth potential with those customers which are looking for messaging as an improvement for their good enough voice products and for whom smartphones are over-serving.

Steven Frank:

Steven Frank:

A lot of thoughtful people, many of whom are bloggers, look at this history and say, “Look at this march of progress! Surely the desktop + windows + mouse interface can’t be the end of the road? What’s next?”

Then “next” arrived and it was so unrecognizable to most of them (myself included) that we looked at it said, “What in the shit is this?”

Highly recommended reading:

http://stevenf.tumblr.com/post/359224392/i-need-to-talk-to-you-about-computers-ive-been

Fraser Speirs gets it:

Fraser Speirs gets it:

What you’re seeing in the industry’s reaction to the iPad is nothing less than future shock.

Very good reading.

Fraser Speirs – Blog – Future Shock

Mini-MSFT:

Mini-MSFT:

Windows Mobile 7: we so dropped the ball in our early phone OS presence that now it seems like it’s a losing battle to have a dog in this fight. But WinMo7 is out there. To me, I can imagine this becoming like the Zune HD: well praised and all, but not making a dent in the market because everyone has already moved on to the iPhone platform.

David Worthington interviews Brandon Watson, “director of product management in the developer platform at Microsoft”:

Watson claimed that many developers of applications for the iPhone OS–which the iPad uses–are not making money. Developing applications for the iPhone and iPad is expensive, he said, because iPhone OS uses the Objective-C language rather than Microsoft’s more pervasive .NET platform. And Apple’s control over the platform has alienated some people that make software for its products, he said.

Now if we can get the Grand Poobah of Ovi to chime in, we’ll be all set.

“In many ways this defines our vision, our sense of what’s next.” – Jonathan Ive

They just signed the death certificate of the PC.

During the reported quarter, Motorola shipped 12 million mobile phones, commanding a global market share of just 3.7%. However, the newly launched two Android 3G smartphones CLIQ and DROID witnessed impressive results. Launched in the fourth quarter of 2009, these two devices generated sales of 2 million units together in the quarter.

Not sure what’s impressive about getting 2 million units sold after $100 million in promotion by Verizon.

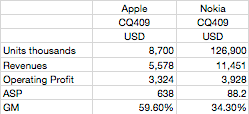

![]() Nokia regained top spot in operating profit. I’ll leave net profit assumptions aside this time, but Apple is sure to have beat by having far lower R&D as percent of sales.

Nokia regained top spot in operating profit. I’ll leave net profit assumptions aside this time, but Apple is sure to have beat by having far lower R&D as percent of sales.

Nokia Smartphones had a good quarter due to new launches. I show also share and ASP comparisons for smartphones in both companies.

I think it’s a logical evolution of mobile computing. A hop along the trajectory. When the iPhone first rolled out as an embodiment of the new touch-based UI–a disruptive technology, I said it was far too good as a phone. It could not be a better phone because phones were as good as they could be. It was a pretty lousy computer so I reasoned all it could become was a better computer. The iPad is a better computer.

I think it’s a logical evolution of mobile computing. A hop along the trajectory. When the iPhone first rolled out as an embodiment of the new touch-based UI–a disruptive technology, I said it was far too good as a phone. It could not be a better phone because phones were as good as they could be. It was a pretty lousy computer so I reasoned all it could become was a better computer. The iPad is a better computer.

Will it be a big hit? I think it will grow nicely and be profitable. It will take several iterations but eventually it will absorb usage from low-end laptops and move computing to new contexts. It will have amazing applications in certain verticals like education, health care, travel and automotive use.

All these steps are like checkboxes in the disruptor’s playbook. In 5 years, this will be as big a business as the Mac and then Apple will have to think how they break out of the 5% share ghetto.

Will there be a response? Yes, but, like with the iPhone, not for a long time, and not symmetrically. The PC guys will dismiss this and the phone guys will see it as outside scope. Once they begin the effort in earnest, it will fall well short of the entrenched, incumbent, integrated(*), rapidly evolving juggernaut that will be Apple Mobile Computing.

(*) Note the emphasis from Apple on its own CPU in the device. Apple does not talk about chipsets in their devices, but they did this time. Not only are they signaling control, but it also shows that value-chain integration down to silicon is what is needed to go up the performance trajectory for good-enough mobile computing.

When asked about the company’s recent acquisitions of Quattro and Lala after yesterday’s earnings report, Apple’s chief financial officer Peter Openheimer answered, “In terms of Quattro and Lala we acquired Quattro because we wanted to offer a seamless way for developers to make more money on their apps, especially free apps.”

When asked about the company’s recent acquisitions of Quattro and Lala after yesterday’s earnings report, Apple’s chief financial officer Peter Openheimer answered, “In terms of Quattro and Lala we acquired Quattro because we wanted to offer a seamless way for developers to make more money on their apps, especially free apps.”

As I said before: why would a developer bother with AdMob if Apple integrates ads into the SDK? Does AdMob offer better terms? Does AdMob offer more sponsors? It’s the developers (and Apple indirectly) who supply inventory.