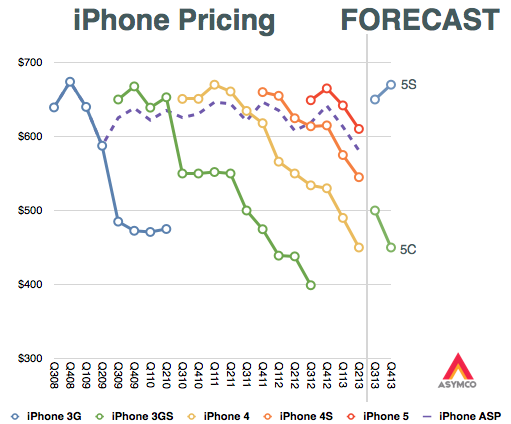

One of the enduring mysteries of the iPhone has been its lack of a portfolio. After six years it seems that Apple has finally acquiesced that there should be one, albeit currently limited to two items. The second enigma is related to the price, namely why does Apple ask so much for its phones? At an average sales price of $600 it’s a shocking premium to the average phone, and with a six year run, a shocking resistance to the corrosive effects of competition.

The obvious answer to why Apple asks so much is because it can. Anybody would if they could. That’s a poor question. So the right question should be: why does anybody pay this much? One could answer that few do and it’s not a mystery that some feel better paying more simply because they can. But those who pay Apple’s prices are, mainly, not consumers. They are operators. Exactly 270 of them.

So then let’s re-ask the question: Why do so many operators pay so much for Apple’s phones? We can’t answer that with the psychological slurs usually directed at the brand. Surely Operators aren’t competing in beauty contests or need to soothe their collective egos. The decisions operators make on whether to range a phone are driven by hard economic realities: ARPU, churn, network costs, depreciation, ROI, etc. Some clearly can’t make the iPhone fit their economic models and indeed about two thirds of them don’t. But the most prominent1 do. DoCoMo, the largest in Japan just did after holding out for five years. Verizon held out for years, as did T-Mobile. China Mobile’s acceptance also seems imminent.

But that still leaves the question of why are those operators who do carry the iPhone willing to pay so much for it? I only assume that their decision process is likely to be rational. Mainly because we have a large enough sample but also because there is a lot of money at stake requiring quite a bit of internal consensus and vetting before committment. We have to conclude that operators place the orders because they obtain value from the iPhone even when it’s priced at a premium to the average alternative.

The question which follows then is how do they obtain value? Continue reading “S is for Service”

- Arguably the most important [↩]