My assumption going into this, sixth iteration, of the iPhone was that we would see the expansion of the iPhone into two distinctly positioned products: a low-end C and a high-end S. The assumption was based on what what we saw with the iPad: the regular iPad and the mini iPad.

By using the iPad as a template, my exercise in August was to forecast what the pricing1 might turn out to be for such a split-personality product.

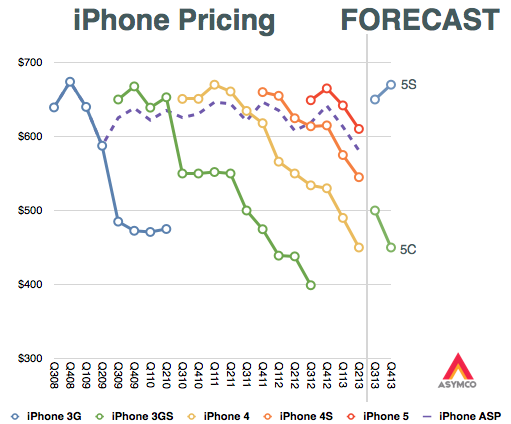

I expected the 5C would replace the “low end” n-2 variant2 and the 5S would continue as the core product. This is reflected in the original graph as devised in mid-August:

The surprise was that the 5C was not “low end” in any way other than having a plastic case. It has a minor spec increase over the 5 but is otherwise a 5 feature set in a plastic skin. It also is priced as if it was the continuation of the 5, with a modest reduction in ASP.

In addition, the continuation of the 4S and 4 (in China at least) means that the old strategy continues more-or-less unchanged.

Knowing the line-up and pricing all that remains to understand is the positioning, or how the products are defined relative to each other.

This is where there might be a shift happening. Under the old model the n-1 variant was meant to be a modest volume contributor to the portfolio, being essentially a cognitive illusion which encouraged buyers to stick with iPhone n at the expense of competitors. However, the new n-1 product (the 5C) has a distinct positioning that makes it seem fresh and not a lesser, stale version of the flagship. It is designed to appeal as a legitimate upgrade for iPhone 4/4S users. It is, in other words, not meant as an illusion, and not focusing attention on the flagship3. Rather, it is meant to be a genuine, core product.

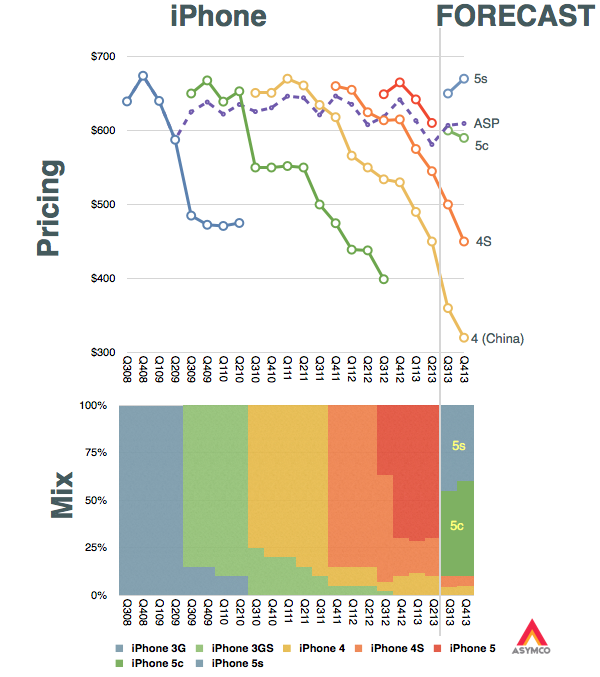

As a result, I expect the mix of iPhones to be more evenly split between the C and S variants. I expect the C to even become the most popular version in the mid-term. My expectations are shown in the following graphs.

There are several implications for this shift in positioning:

- Apple is recognizing that the market is actually “segmentable”. This is the notion that one size does not fit all–a radical idea for the brand. Its mechanism to address it is a “good+better” portfolio. Note that this is not at all like the iPad where the Mini is actually suited to different tasks. The iPad can be thought of as a “small+big” portfolio. The iPhone shows a clear delineation within the same product.

- It is signaling that the premium may be more than what the mainstream needs. This is a corollary to the segmentation implication above but stands on its own because it also implies that the iPhone C is “good enough” and the S is more than good enough (or, to spin it another way, it is for “more demanding” customers.) It also implies that the premium “S” version will be a lower volume contributor.

- The third implication is that the basis of competition is shifting.4 The shift is toward competing for late adopters in advanced markets and with early adopters in trailing markets. The new C model is still not suitable for trailing markets as it still over-serves and is over-priced5, but it is at least signaling the “end of the beginning” phase in the smartphone market.

In summary I’d say that the C signals the beginning of the “good enough” phase which was also evidenced by the increasing mix of the older models during the last year. Financially it shows up as lower ASP, which, as the graph above implies, I expect to drop to $600 and lower during the next year. Margins may not be affected much as the C is still very highly priced relative to its cost of production.

Finally, if the good enough alternative is being “pinned” by Apple as the mid-range it also begs the question of why there isn’t a specific “low end” version. It took six years for Apple to fork the product into two variants. Maybe it will take another year for it to stretch to a third.6

- Revenue/unit to be more precise [↩]

- Older by two generations as the iPad mini replaced the iPad 3 [↩]

- It might still be an illusion for many but I’m suggesting that it won’t be for most. [↩]

- It has always been expected to shift, but the timing is where all the value is captured [↩]

- This post deals with the iPhone portfolio structure or the placement of iPhone models relative to one another. It does not deal with a separate question of why the overall pricing is so high. That question needs to be dealt with as a discussion about the jobs iPhone is hired to do and by whom. I’ll re-visit this job-based segmentation of the market in a future post. [↩]

- For more on the subject see S is for Service. [↩]

Discover more from Asymco

Subscribe to get the latest posts sent to your email.