From the way Apple reports its revenues you might think that the company has several operating segments. There are the iPhone, the Mac, the iPad for which units and revenues are reported. Then there are Services and Other Products for which we have revenues only.

Services is a collection of all non-hardware revenues and is (finally) being recognized as a non-trivial business. With reported revenues of $26.6 billion in the last twelve months, it’s big enough to be a Fortune 100 company and set to double in four years.1

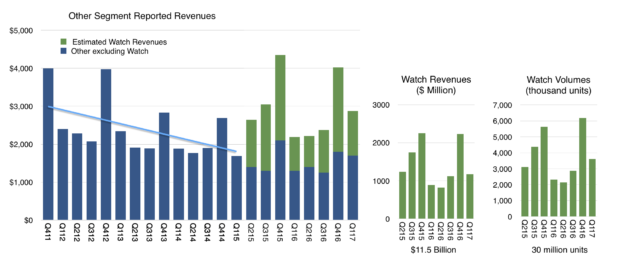

That leaves “Other Products” which now becomes the revenue segment that is “most likely to be ignored.” This segment had revenues of only about $11.5 billion in the last 12 months which would place it at only a Fortune 245 ranking, equivalent to a Toys “R” Us or Biogen. How should we value Other Products?

Other includes many hardware products including iPod, Apple TV, Beats, Apple Watch, AirPods and, soon, HomePod. Each is a significant product, with Watch probably the largest single contributor. But since we don’t have specific unit numbers, we are left guessing at the contribution of each.

The Watch itself has been a point of scrutiny as it could be initially teased out of the mix through an observation of the before-and-after launch vs. trend-line as shown below:

This separation of Watch became harder to discern after the launch of AirPods. Though they are still very hard to obtain, they might be “moving the needle” by now with a contribution that would muddy the Other category further. Same with updated Beats headphones.

This separation will be harder still with the launch of HomePod later this year. This product is priced at a point similar to the Watch and the quantities sold will be very hard to estimate without Apple’s revealing of actuals.

Fundamentally however, all the “Other products” will have a common relationship to the iOS and MacOS hardware: attachment to and integration with a “parent” platform. Apple TV might be stand-alone but I strongly doubt there are many sold into offices or households which don’t have iOS usage.

This means that “Other Products” are very similar to “Services” in that there is a dependency on a primary platform and, as it has been argued, they are therefore fragile. If the core platform declines then the Services and Other Products decline as well.

Given this dependency it makes little sense to carve these categories out as separate businesses. They cannot stand alone. They are very much the “children” of the parent platforms.

This is why it’s assumed that Services, (a Fortune 100 company) and Other Products (a Fortune 250 company) can be discounted to zero. By focusing attention on the iPhone one can capture all the essential value of Apple. This is in contrast to the “sum-of-parts” valuation that could be applied to a set of independent business units in other companies.

And yet I started this discussion with the point that you might be tempted to look at Apple on the basis of these reported revenue segments. The choice of what Apple reports is arbitrary. It could report no segment revenues at all and publish just one revenue number. This is roughly what Google Amazon and Facebook do. Or it could report segments in some other way. For instance, app store revenues and AirPods could be reported as part of “The iPhone Division”. Or maybe it could bundle all iOS devices and services and accessories into another segment called “The iOS Group”. Or it could create a “Devices group” and a “Personal Computing” group. Microsoft famously shuffles its revenues into creative segments based on various organizational structures or choice of what it wants to project as its focus.

There is no limit to the ways Apple could slice revenues into segments. The reason Apple does it the way they do is mostly due to historical reasons. The company used to report the iPod separately as a segment but it no longer does. It also used to report Software separately, because, presumably, it charged for it but now it no longer does. It also separated laptops or portables from desktops.

The current reporting system is tempting us to draw certain “business unit” conclusions. These boundaries are illusions because Apple does not have business units. It has only one Profit and Loss statement (P/L) and is organized functionally. There is no “head of iPhone” or “head of Mac” responsible for each siloed revenue and cost structure. Instead, the entire business should be seen as a whole because it is managed as a whole.

This is easily evident in how the products are designed and marketed and how they are engineered. The iPhone may spawn AirPods and AirPods may have no value outside the iPhone but the iPhone is valuable precisely because it has AirPods and Apps and Music and iCloud. And Apple TV, and HomePod and whatever comes next. The reason the iPhone can be sold at three times the price of competitor products is because of the Services and Other Products and iPad and Mac symbiosis. This integration drives the satisfaction, loyalty, price and brand value. There there are the Apple Stores and the launch events and the countless details that make up the ownership experience.

The fact is that you can’t slice and dice Apple.

There is one Apple and it must be analyzed as a unitary entity. That analysis is therefore difficult. It is easy to pick up the numbers given and study them in isolation. The iPhone, the iPad, the Mac. We all do that.. However we miss a great deal in doing that.

The lesson is that data we obtain leads us to see something but it also blinds us by taking attention away from what we cannot see. All data lies by omission. That which is left unmeasured may be where all the truth lies.

- Although a non-zero business, the valuation of Services continues to confound observers who cannot separate it from the hardware businesses it attaches to–which themselves are considered near commodity value–thus paradoxically valuing the overlying asset of Services near or precisely at zero. Incidentally, Facebook is Fortune 98 at $27.3 billion and it is also one of the top 5 largest business by market capitalization. [↩]

Discover more from Asymco

Subscribe to get the latest posts sent to your email.