I’m pleased to announce the next Apple investor event, taking place on Tuesday, June 10, 2025, timed to coincide with Apple’s Worldwide Developers Conference (WWDC25).

ACTIVE: The Apple Investor Conference

ACTIVE is an in-depth examination of Apple as a business. The event is designed for individual investors, analysts, developers, and others with a stake in the Apple ecosystem. We move beyond the headlines to analyze the company’s operating model, portfolio of products and services, competitive position, and strategic trajectories. We will examine how Apple may navigate emerging macroeconomic volatility, evolving AI dynamics, and a shifting regulatory environment. Participants will also get a sneak peek at a new predictive modeling for Apple’s performance.

Topics we’ll cover:

Financial Performance: Trends in revenue, margin, and customer value

Valuation Logic: From users to markets to multiples

Platform Dynamics: Hardware, software, and services in sync

Global Levers: Tariffs, China, supply chains, and macro forces

Strategic Maps: The next S-curves and adoption inflection points

Externalities: Regulation, risk, and reputational capital

Competition: Platforms, partners, and substitutes

We’re preserving the tight-knit format that makes the event special—limited in-person seats and deep interaction. For those unable to attend in person, we have arranged for a worldwide livestream. Remote participants will be able to view live presentations, pose questions, and engage in discussions in real time.

We hope you’ll join us—in-person or via livestream.

ACTIVE: The Apple Investor Conference

Tuesday, June 10, 2025 (the day after the WWDC25 keynote) Boston (in-person) & Worldwide via Livestream

Learn more and register at ACTIVEconf.com. Early bird tickets are now available. Use code asym27 for an additional discount.

According to JP Morgan analyst Samik Chatterjee, citing Sensor Tower, Apple’s App Store revenue for May 2025, increased by 4.9% month-over-month (which compares to an average sequential increase of 2.3%) and an acceleration of year-over-year revenue to 13.0% in May versus up 11.8% in April. On a year-over-year basis, the App Store downloads increased by 3.1% in May (versus +5.8% in April) according to Chatterjee.

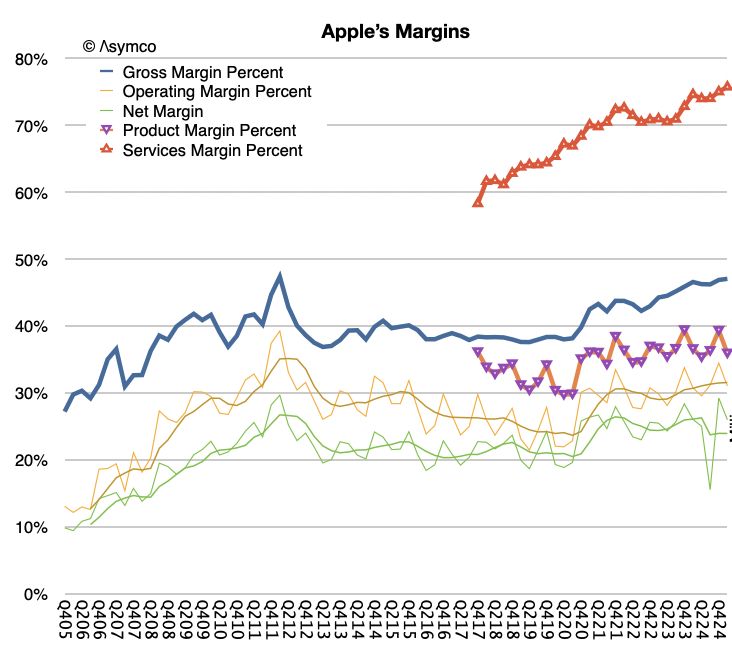

This analysis is based on app download sampling and may be indicative of the activities of consumers on the App Store. Services revenue in the first calendar quarter was $26.6 billion, up 12% year-over-year and at an all-time revenue record. Services gross margin was 75.7%, up 70 basis points sequentially, also an all-time record.

The world however seems to be having a problem with Apple Services. After years of skepticism of its relevance, now that it has achieved a run level above $100 billion/yr., it’s being criticized for being harmful to competition.

The comments that it’s unfair to developers or that it deters innovation are uninformed to say the least. What is missing from that analysis is that the App Store is only a small fraction of the entire ecosystem around Apple’s platforms and that the economic activity the platforms enable is immense.

Let’s learn.

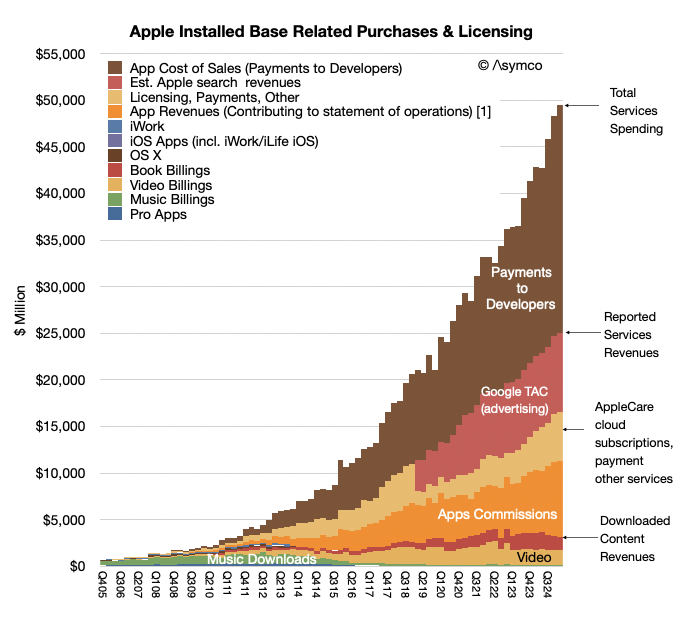

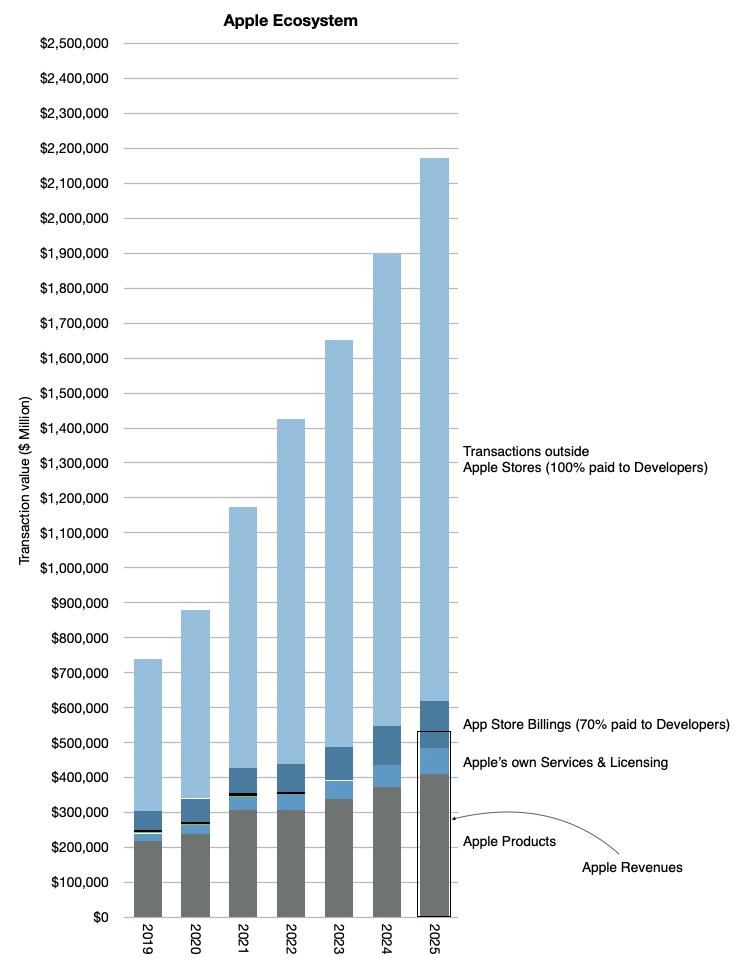

Over the last year Apple reported a bit more than $102 billion in revenues for Services at a very high margin. The reason it was such a high margin was partly due to the fact the Services does book all payments from customers through the App store as revenues. In other words it does not include payments to developers as either revenue or costs. Those payments pass through but they are certainly part of the economic activity on the store. It would be indeed unusual for a physical store not to report what it pays for what it sells as part of revenues. But this is the basis Apple chose (or was obligated to choose) as the way to report App Store revenues.

Thus considering the payments to developers, the economic activity directly related to the App Store amounts to $120 billion/yr which includes commissions of about $30 billion/yr (last 12 months) and payments to developers of about $90 billion/yr (implying about 25% blended average commission rate.)

So including payments to developers the Services business grosses $186 billion/yr. of which 102 billion is reported as revenue, with the 75% gross margin and $90 billion is paid to developers “off the books”.

But that $102 billion in revenues is only about 30% App Store commissions. The rest includes many types of income: It includes:

Advertising which consists of Apple’s own advertising services and third-party licensing arrangements notably the distribution fees for Google search (accounting for most of Googles “TAC” or traffic acquisition costs.

AppleCare, Apple’s own extended warranty service.

Cloud Services which provide content synchronization.

Digital Content which not only includes the App Store but also stores for books, music, video, games and podcasts. Apple also offers digital content through subscription-based services, frequently bundled, including Apple Arcade, essentially a game subscription service; Apple Fitness, a personalized fitness service; Apple Music, which offers music streaming and on-demand radio stations; Apple News, a subscription news and magazine service; and Apple TV, which offers exclusive original content produced by Apple and live sports access licensed sometimes exclusively by Apple.

Payment Services which offers Apple Card, a co-branded credit card, and Apple Pay, a cashless payment service.

The quarterly view is summarized in the graph above. So a fixation on the commission is only a view into 16% of Services as an economic foundation (the orange area in the graph above).

But that’s still only a sliver of the whole picture.

A report written by Jessica Burley, Analysis Group and Professor Andrey Fradkin, Boston University Questrom School of Business has estimated that the global App Store ecosystem facilitated $1.3 trillion in developer billings and sales in 2024. As the report writers say: “For more than 90% of the billings and sales facilitated by the App Store ecosystem, developers did not pay any commission to Apple.”

How is this not visible? The reason is that this economic activity is distributed over the millions of purchases Apple users make through its iOS Apps every day. This includes traditional App Store “Billings” including paid downloads and in-app purchases, including subscriptions, that use Apple’s in-app purchase system and “Sales” which includes money spent by customers purchasing goods and services in general using any iOS and iPad OS apps. Apps developed by Apple such as Apple Music, Safari or browser apps such as Chrome are excluded from this analysis.

The economic activity unleashed by the App Store now reaches well over $1.3 trillion/yr. As the authors further explain,

While the present analysis captures the major app monetization strategies available to developers, the full economic impact of the App Store ecosystem extends beyond the estimates provided in this report, as the current methodology does not capture all of the ways in which the App Store ecosystem facilitates sales, or all of the benefits created by apps. For example, the App Store supports “companion apps” that raise the value of a company’s goods and services, including smart home apps and health apps. In addition, many apps now use different monetization strategies. As such, this analysis does not account for all the ways in which the App Store ecosystem creates value.

Furthermore the report breaks down the categories as Digital Goods and Services, Physical Goods and Services, M-Commerce (General Retail, Travel, Food Delivery and Pickup, Grocery, Ride Hailing), Digital Payment and In-App Advertising.

In addition the report estimates these categories from 2019 as well as 2024 providing a growth perspective: Over the past five years, the App Store ecosystem has more than doubled in size, increasing from $514 billion in 2019 to nearly $1.3 trillion in 2024.

It also identifies regional dynamics between the US, China, Europe (with select countries) and Rest of World (with select Asian countries).

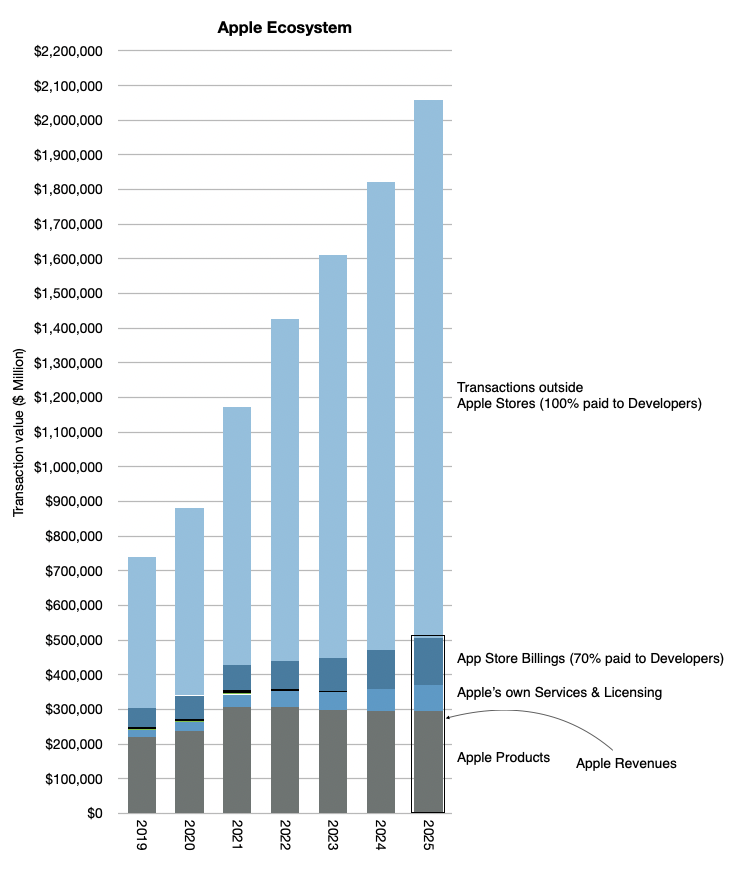

I’ve been keeping my own analysis of what I called the Apple Economy and it includes these transactions outside the App Store and Apple’s own products and services. If I were to subtract Apple’s own revenues from the total, for 2024 I was getting about 1.4 trillion (out of a total of over 1.8 trillion).

My point was always to estimate the economic impact of Apple beyond its own sales. This gave us perspective to assume that in 2025 the total would reach over $2 trillion. The graph below gives the perspective which also implies a doubling since 2020 to 2024.

The new report from Burley and Fradkin is a detailed, bottom-up analysis which quantifies what was perceived as the economic value of Apple being far more than what the financial data records.

Bill Gates once stated in reference to Zuckerberg’s assertion that Meta was developing a “platform” that it’s not a platform unless the economic value of everybody that uses it exceeds the value of the company that creates it.

Apple captures about $30 billion as sales but delivers over $1.3 trillion in sales, a multiple of 43! I would call that generous. In addition it doubles the market in 4 to 5 years. I’d call that market expanding not constraining. Finally, it’s a market that Apple created out of nothing. I’d call that market creation not destruction.

If judged on the question of creation and satisfaction of the customer, i.e. the ultimate purpose of the firm, the App Store and Services in general has satisfied 1.4 billion people. That they are spending over $1.3 trillion and doubling in 4 years is nothing short of astonishing.

We’ll discuss this topic and other topics related to Apple at ACTIVE: The Apple Investor Conference, which takes place on next Tuesday, June 10th, the day after the WWDC25 keynote.

Apple’s relationship with China has always been a point of worry for investors. Nine years ago Carl Icahn sold his entire stake in Apple due to China fears. In April 2016 Reuters reported that “Icahn had been a huge cheerleader of Apple, acquiring a stake in the company almost three years ago, repeatedly calling the investment a `no brainer.'” In an open letter to Apple Chief Executive Officer Tim Cook in May 2015, Icahn had argued that shares of the iPhone maker were worth $240 ($60 split adjusted), about 90 percent more than they had been trading. At $240 a share, Apple’s market cap would be $1.4 trillion, Icahn asserted. But Icahn, who owned 45.8 million Apple shares at the end of 2015, said China’s economic slowdown and worries about how China could become more prohibitive in doing business triggered his decision to exit his position entirely.

Icahn’s stake when he acquired the shares was worth nearly $3 billion and he sold it for about $5 billion. A $2 billion profit. But China worries kept him from holding until today when his shares would have been worth $36.6 billion, thus foregoing $31.6 billion in profit.

Leaving $31 billion on the table (not including dividends) seems a high price to pay for a misidentified anxiety on China.

The public reasoning was: “But you worry a little bit, maybe more than a little, about China’s attitude.”The Chinese government could `come in and make it very difficult for Apple to sell there … [They] can do pretty much what [they] want there,’ Icahn said. Earlier [that] month, China shut down Apple’s iTunes movies and iBooks stores within the country, following Beijing’s introduction of regulations in March 2016 imposing strict curbs on online publishing, particularly for foreign firms.”

That was 2016. Today the concerns appear to be:

Slowing sales due to rising competition from Chinese brands

Slowing sales due to Chinese economic slowdown

Tariffs and other barriers to trade affecting pricing in the US

Geopolitical threats to supply chain, including processor manufacturing in Taiwan

Should today’s investor worry about China more or less than Icahn did in 2016?

In the case of competition in China, we have to understand that China does not have a free market or “laissez-faire” economy. The clue would be the middle “C” in CCP which, importantly, has a monopoly on political power in China. In spite of an ideology hostile to private property and market economics, the fact that Apple not only is allowed to operate in China but also is the market leader in urban (read: wealthy) areas and indirectly employs millions of workers and empowers millions more developers should be seen as something of a miracle. It continues to operate only insofar as the CCP allows it to continue and the CCP is nothing if not calculating. Clearly, China has seen Apple’s presence in the market (both as producer and seller) as beneficial. One could argue about who benefited most but overall deals happen (and persist) because both parties benefit.

The competition has been improving lately, but when has it not?

Fundamentally, from the consumer point of view, the competition question is moot since the alternatives are not iOS. The iOS ecosystem is incredible from a value-generation point of view, and Android has been clearly contained as a threat. (A nostalgic footnote. Recent talk of Alphabet being forced to sell Android is a wonderful reminder of the question I asked many, many years ago: why should a search engine need an Operating System (or a browser), but more about this later).

Chinese macroeconomic worries are not new (see Icahn’s from 2015). In most economies cycles are natural but in China there has been such a long expansion (since at least the 1990s) that a slowdown is considered a huge threat to stability. A recession would be seen as an existential threat. The CCP intends to manage its way through economic stress—one of the defining aspects of their semi-controlled economy is that “the state knows best” and markets can and should be controlled. This won’t last but the consequences are not likely to be catastrophic. China’s economy is probably large enough to avoid sharp changes which gives management enough time to muddle through. I would not say that this worry is unwarranted but rather that the changes are gradual enough to allow for some strategic planning.

The Tariff question has been partly touched on in a previous post. But the flip-flopping on the topic suggests that it’s a bargaining method similar to holding a gun to your head while threatening someone else that if they don’t do what you ask for, you’ll pull the trigger. Then relenting when they say nice things. Then repeating it.

Tariffs do not affect the customer relationship with the brand.

In 2016 Icahn’s worries were not geopolitical (they were just political) but has the world become more unstable since? The Covid pandemic was the trigger for much of this instability and we are still dealing with the consequences globally. However the bigger forces behind global changes are demographic and the subsequent loss of growth in China (and Russia) are causing authoritarians to find external threats to stay in power.

This will not play out quickly. There are worries but we should consider China (and India, and Africa) as sources of non-consumption that can and will be addressed with production. So the worry here is again structural and slow-burning. I would argue decades in the making.

Not much has been said about the benefit to Apple of its China strategy. Many assume that lower costs and access to a large market are all that has been gained. But it’s much more complex than that. The access was not to a lower cost base but also a much more agile and flexible production infrastructure. The flexibility allows for a very tightly coupled value chain. The result is a reduction in inventory and a rapid time-to-market which is essential to Apple’s integrated product/software/service rhythm of yearly launches.

I’d argue that without the flexible, at-scale production system China allowed Apple would not have been able to succeed at reaching a billion highly satisfied users. The world would have been awash with cheap Android phones and very few iPhones, a repeat of the PC model where hardware was largely irrelevant.

The challenge of the future is to take this model globally and either transplant it to India and other places or to scale it in such a way that it can be distributed to many centers of production. Toyota famously not only created a product system that reduced cycle time and inventory but did it with 400 plants globally. I certainly hope that the Apple Production System will also be celebrated one day as the “machine that changed the world”.

Come learn more about the Apple Production System at the ACTIVE conference.

In my last post I asked if tariffs, antitrust remedies, distribution dissatisfaction and non-iOS competition make any impact on how customers perceive the company. Let’s begin with tariffs.

Broadly, tariffs are unpredictable and politically arbitrary. The greatest harm may come not from the misallocation of capital among nations but from the inability to plan and thus the non-allocation of capital altogether. A cessation of investment is a recipe for stagnation if not poverty but it’s not a management challenge. In most situations it behooves every manager to do nothing. Therefore it’s no more interesting to devise a strategy for tariffs as it would be to devise a strategy for volcanic activity.

But still, how does it affect the relationship with the customer? One could argue that tariff-induced price increases might cause a decline in demand but there are always going to be alternatives for consumers. Let’s not forget that tariffs are being offered as punishment for US customers only and the US is less than 40% of Apple’s business (“Americas” is about 42% and that includes Canada, Mexico, Central- and South-America.) The rest of the world has already been punished to varying degrees with higher prices due to customs fees, value added and other taxes. This is why there was a thriving smuggling pipeline from the US to rest-of-world for as long as Apple has been in business.

The smuggling of products across borders without payment of taxes on trade is called the grey market and is neither new nor small. The grey market for electronics is estimated to range from 6% to 8% of the global market, worth up to $60 billion. Some studies suggest that 13% of global consumer sales involve products sold outside the manufacturer’s intended market with the electronics segment above 14%. The share of Apple sales generated through grey channels may be somewhere in the upper part of that range.

Even 10% of Apple sales being grey market could come as a shock to many but it shouldn’t. Many Americans may be unaware of this because the US has been the source of grey exports with couriers smuggling products from there to almost every other location on earth. This is mainly because the US is among the least taxed consumer products markets.

Perhaps the pipeline will soon reverse direction.

American couriers queuing in foreign Apple Stores hoping to bring home some “duty free” iPhones or doing it for friends, family or for a fee is certainly foreseeable. Prohibition era alcohol smuggling was a vast industry for the US, mainly from the Caribbean and Canada. Drug smuggling has been a vast industry since then. Consuming contraband is therefore not beneath US consumer dignity. Organizing this on a large scale enables criminal gang formation and it might appear harmful for a brand to be associated with such activity. But again, reflecting on this historically, it does not normally detract from the brand that it is the subject of smuggling. Marlboro, Dewars and other toxins retained their cachet throughout their smuggling to and from various markets. Firearms, tobacco and alcohol are as desirable now as they were when constrained to the point of exclusion.

When I was young it was common to see Levi’s jeans and boxes of American cigarettes being used as currency behind the Iron Curtain and nobody would argue that those brands suffered as a result.

Today, even with higher prices, satisfaction among non-Americans is not worse than with Americans, taxes and governmental pilfering notwithstanding. In other words, prohibitionism does not work in eliminating demand or brand value. Tariffs are a mild form of prohibition and therefore their value impact is quite limited.

It’s not unusual to see articles consisting of lists of reasons why Apple is facing an existential crisis. Agonizing and hand-wringing about Apple been a meme for decades, so much so that it had its own web site, The Apple Death Knell counter and the “Pray” for Apple imagery was a thing since the 90s. The original article from June 1997 offered 101 tips on saving the company starting with outsourcing hardware or scrapping it entirely.

Although the imminence of death has always been persistent, what’s changed over the years were the causes. There are far too many to recall or enumerate but I have through personal recollection and pattern recognition grouped them roughly into three categories:

Irrelevance due to low market share, i.e. insufficient network effects for its platforms which will eventually drive users away. This is fundamentally a size problem.

Insufficiency in capital/resources/talent/management. This includes the death of Steve Jobs, the departure of various other managers and historically the low spending on R&D. This is more qualitative but still fundamentally a problem of being too weak.

Externalities including but not limited to: law suits, regulations, taxes, technology standards. This includes everything from the absence of the Beatles in the iTunes store to confiscation of assets or extortion by governments. Extreme versions are antitrust cases alleging monopoly status. This is a problem of being too big or too strong. (Contrast with the first two categories)

For instance, during the last Apple Investor Event, I highlighted a typical article citing a list of problems for Apple. It was Titled “5 problems facing Apple it won’t talk about at is April event”. Published in August 2024 it cited the following:

Maintaining profitability. Citing a drop in operating margins in 2020(!) the problem was stated as a need to maintain momentum.

Antitrust regulation. Citing EU and US investigations against Apple and other Big Tech companies. Money quote: “reports have surfaced that several tech companies in China are actively testing ways to circumvent Apple’s new privacy update”).

Lawsuits in general, Epic trial in particular.

A lack of diversity in the management team. Essentially, insufficient DEI.

Competition. Google, Blackberry, Dell, Fujitsu, Microsoft and Samsung are cited.

When I read this I thought it must have been AI generated (hallucinated more likely). The dates did not make sense (August publication predicting an April event) and the competition cited was obsolete (Blackberry? Fujitsu?). It was a random list of Apple news framed as problems. Rather than try to refute them, I realized that it did not matter. The objective of the author was not to illuminate but to discharge something, anything, as long as it was negative.

Since last August a lot has happened. A new US administration, a new set of problems. Judging by the share price and news flow, Apple bashing is once again in vogue. (Incidentally, the stock price reached an all-time-high in December 2024 at nearly $260/share, a substantial increase from $170 or so six months earlier.) Today everyone and their editor is jumping into the scrum writing lists of Apple problems.

The pattern however seems a bit different this time. Almost all the catastrophes Apple has are externalities. Let’s try to enumerate them (inspired by Bloomberg.)

Tariffs. Consequences include presumably negative impact to company’s operations, product development and device prices.

Antitrust. A US Department of Justice lawsuit for allegedly anticompetitive practices. Similar actions by the European Union, South Korea, Japan, India, etc.

Lawsuits. Apple must stop taking a commission on in-app purchases and subscriptions paid via the web. Epic again.

Distribution deals (Google antitrust). The threat of losing a $20 billion-a-year deal with Google for default search placement.

AI delays: the risk of falling even further behind its tech peers

Competition in China.

What these examples seem to share is that, except for the AI execution, they are externalities and thus of the third category. They are therefore problems related to being too successful.

Tariffs are a problem because Apple relies on massive scale and thus requires integrated production which creates concentration in production centers which are difficult to redeploy. Antitrust is a problem because Apple is too big and thus dominates developer distribution. Lawsuits center on having too much control—related to antitrust. Google antitrust remedy forces a decline in distribution revenue for browser search—a predicament coming about Apple’s enormous leverage vis-a-vis Google. Being so big means there is only one way to go: down, hence Chinese competitors gaining share. Lastly, AI execution problem is more Category 2 problem but would not be an issue if Apple did not insist on Privacy for its customers, something which caused much of its success with customers that it got too big.

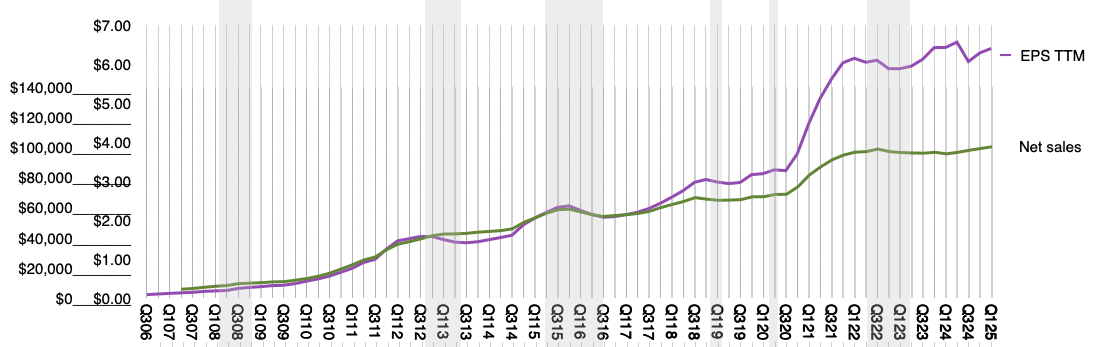

Incidentally, profitability is now higher than ever, top line growth is consistent, bottom-line growth is even faster, the company is guiding growth in-line with current trajectory, the number of customers is at a new record, churn into the platforms continues, Apple is winning against non-consumption, capital is pouring into shareholder pockets and R&D spending is soaring. Cue the charts.

What the casual observer might note missing from the Doomed listicles is any mention of customer satisfaction, loyalty, acquisition and retention. The things the company actually talks about on earnings conference calls.

Do these externalities of tariffs, antitrust remedies, distribution dissatisfaction and non-iOS competition make any impact on how customers perceive the company?

We’ll discuss this in the next few posts, as the lead up to presentations at ACTIVE: The Apple Investor Conference on Tuesday June 10th, the day after the WWDC25 keynote.

Apple Investors are keen observers of metrics of financial performance. We have to track top line, bottom line and many lines in between. Updates to the data are delivered every quarter through official documents such as the 10K and statements made in conference calls. These data are then analyzed and opinions are formed on the viability, sustainability, and prospects for the company.

The community of investors changes rapidly, with shareholders able to enter and exit with a click of a button. All it takes is capital. Therefore many critics of shareholders as stakeholders point out how fleeting the commitment can be. Though there is skin in the game in the form of committed capital, there is no requirement for staying committed.

This is not the case for another set of stakeholders. In a previous post I pointed out how important employees are to the company and my belief that their commitment is probably management’s greatest concern.

But if one were to sum up the total population of a stakeholder group multiplied by its required level of commitment, there is a case to be made that the most vested community is that of Apple’s developers.

This group numbering in the millions makes an enormous contribution to the prosperity of the company and indeed of the other stakeholders. And they do so through tremendous personal risk. If you are a developer you know this, but perhaps other stakeholders do not. So let me elaborate.

An Apple developer must spend years becoming versed in the developer tools, purchase membership and equipment, navigate getting their software accepted and hope that someone, anyone buys the result. Afterwards, they need to maintain the code and update it frequently as the underlying software and hardware changes.

This adds up to enormous personal opportunity costs. Developing means not doing something else and developing for Apple means (typically) not developing for some other platform.

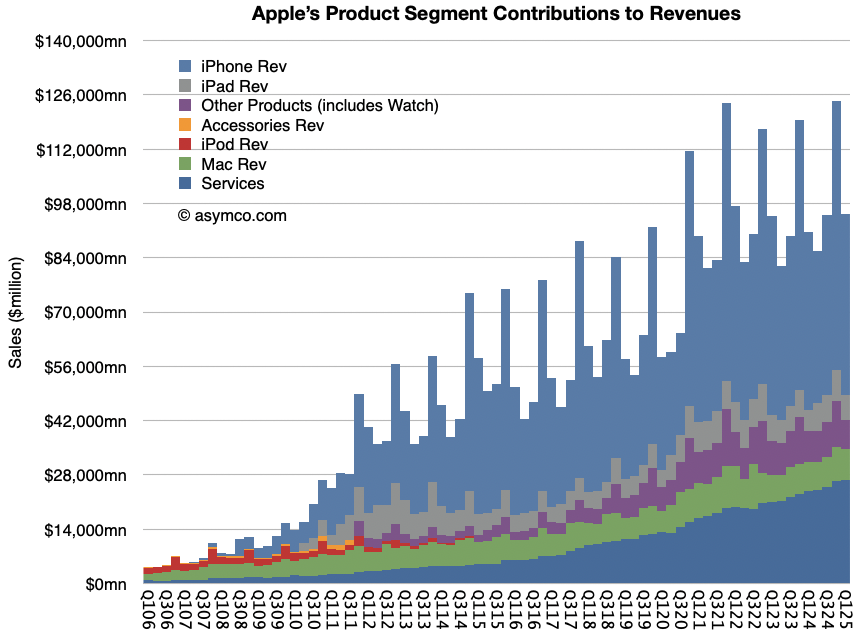

The benefits can be significant however. Apple publishes the amounts paid to developers. That is part of the graph shown below.

The dark blue area shown as “App Store Billings” includes about 70% paid to developers which I would estimate at about 100 billion in 2023.

But these are direct payments based on App Store transactions. A great number of transactions and economic activity takes place outside the App Store. That is over $1.1 trillion in 2023. It should grow to over $1.3 trillion this year.

And then there is AI. As Ben Bajarin and I discussed recently, the integration of AI is shifting the risk/reward equation for developers to include capital spending or monetization of computation itself.

A lot is at stake. Not only in terms of upside but also downside. Developers need to understand the “state of the union” for Apple as a platform and ecosystem from a financial point of view. Conversely, investors need to understand the degree of dependence and commitment being made by the developers.

There has been no forum for this to happen. Until now.

At the first Apple Worldwide Investor Conference ( WWIC ), we will bring together individuals with a stake in Apple’s future—investors, analysts, and developers—to foster a meaningful conversation about Apple’s ecosystem, and a better understanding of Apple as a business.

The event will take place on September 19th, in-person in Boston with limited seating, and via remote livestream globally, where you can watch, ask questions, and discuss, live.

Tickets are available now. Asymco followers can get an additional discount using code asc24.

It’s Labor Day in the US (and Canada, though not anywhere else where it’s celebrated on May 1st.) This would be a good time to discuss Apple’s primary challenge.

Writers whose unfortunate job is to cover Apple inevitably put forward lists of “challenges” faced by the company. It really is not possible to write or speak about Apple without manufacturing one’s own list of problems, obstacles, difficulties, rising competition, inevitable transitions, strategic failures, and the lack of innovation.

For instance, as recently as a week ago, in an article announcing the change in CFO, a pundit noted that “[the new CFO] Parekh’s main challenge will be navigating ongoing antitrust lawsuits. ‘These are challenging times for Apple on multiple fronts’, citing increased regulation, EU scrutiny, and growing competition in China.” Challenging times for Apple. Surely not like previous times which were not challenging at all.

I Googled “challenges facing Apple” and top hit was a list from CNN dated January 25, 2024. The tag line “It’s only a few weeks into 2024, and Apple’s year ahead is paved with trouble.” A discussion of its doom in China is followed by an Apple Watch ban challenging Apple “reputation”. Surprisingly, being behind on genAI and the existential crisis AI will bring only showed up third. Then came “revenue concerns” because of reasons and finally, being a regulatory target around the world rounded out the top five.

Clearly, repeating this exercise every few weeks would allow an entirely new list to be created with a completely fresh dose of dread. As the previous list fades in memory a reminder on your iPhone should get the list generation started on time. [AI only makes this easier.]

But what none of these lists seem to include is what I consider to be Apple’s primary worry. I believe this is the one thing that keeps Tim Cook awake at night. This being the preservation of employee morale.

As evidenced by what I get as questions and what is enumerated endlessly, what most people don’t understand is that Apple is exceptional because of the combination of culture and talent and not the particular circumstances it finds itself in. Listicles of circumstances are easy to generate but a good management system is resilient to circumstances and indeed anticipates them or makes their own. The thing that Steve Jobs built was a mechanism that converts the talent and dedication of great people into product that is genuinely adored by the people who use it. That mechanism is beyond a set of rules. It’s culture.

“Build” culture sounds far too vague and simplistic, but the reality in almost all other (large) organizations is that almost all talent is wasted. That primary asset, its employees, is perhaps less than 10% applied to the benefit of users. Much of it is wasted in politics, frictions, pointless disagreements, burning out, and what I call “creative inefficiency”. If Apple could just waste only 60% of its employees’ contributions it would be four times better than average and probably be the most effective company in the world.

Culture is what makes the application of talent effective and efficient. It is the magic sauce. And losing that culture would be the greatest existential threat to the company.

So on Labor Day our reflection should be on how to keep what is now a very, very large organization meaningful to each and every employee. The CEO’s efforts should be prioritized on customers first but employees second (and shareholders at best, third). This means inducing employees to be creative and productive and keeping them in that state of “flow” for the duration of their employment. For top management it’s even necessary to keep their loyalty and dedication *after* their employment ends.

The methods vary and are some of the most secretive aspects of Apple. As I said many years ago, many want to copy Apple’s products but few want to copy being Apple. That is mostly because few even know what Apple is and how it works. Having said that, I would like to put forward some observations on “the Apple way” of management.

1. Provide incentives for employees to stay in the same functions as long as they continue to improve their skills. This means focusing on becoming better at their craft rather than “grooming” them for climbing the corporate ladder.

2. Preserve a functional organization. Obviously this means avoiding market-driven or matrix org structures.

3. Tap individuals to become managers only if they exhibit management skill. This is far harder than it seems. Few highly talented individuals in a particular area of expertise want to give up practicing in order to become a general manager.

4. Avoid political in-fighting by maintaining separations between functions and deciding budget allocations through a centralized process. This avoids “empire building” (and its corollary of back-stabbing) through budget and headcount accumulation.

5. Top management should be deeply aware of all aspects of the business. This means keeping the business fairly narrow, with a short list of products and services. Narrow focus needs to be coupled with a wide base of applications. In other words, pick products and services which have broad appeal but keep their number low.

If you read this correctly, you will note how diametrically opposed this is to the modus operandi of corporate entities. It really is asymmetrical to how management is practiced and that leads to an outsized competitive advantage for Apple.

In November of last year I wrote a series of posts regarding the relationship between Google and Apple in light of the antitrust trial that Google was facing. The expected verdict was issued (Google was declared a Monopolist and found to be abusing that position). Many more appeals will follow and a remedy will need to be agreed upon–a process which will take many years. The implementation of any remedies will take yet more years.

Nevertheless, commentary on this trial has continued to center of the harm the verdict will do to Apple. Since Apple receives a substantial amount of highly profitable revenue from Google for search defaults, the conventional wisdom is that, due to this verdict, Apple is at a very high risk of losing that revenue. Very little has been said about what harm the verdict will do to Google. The paradox to me is why there is no connection being made between the implied loss to Apple being necessarily a gain to Google.

Since almost all people will continue to use Google on Apple devices, regardless of default, not paying for distribution (through defaults) will lead to a huge boost for Google’s bottom line. In other words, most comments currently imply that a verdict declaring Google an abusive monopolist will result in a huge benefit to Google. So I ask again: why would Google management fight against such a verdict? Surely it would have been far more beneficial to argue to lose rather than to win this case! The court will force Google to make more money.

But my conclusion last November was that “a declaration that this [default placement] deal is invalid simply means that Apple and Google would craft another deal that would work around the restrictions. And that new deal would probably turn out to be more beneficial to Apple. [and less beneficial to Google.]”

The reason would be that Apple would increase its bargaining power because Google has, necessarily, decreased its own by losing the case.

I’m thrilled to announce the next Apple investor event, September 19, 2024. Henceforth the events will be called the Apple Worldwide Investor Conference (WWIC). WWIC will examine Apple’s business in-depth using the latest data. In addition to financial review, we will also cover technology, externalities, company culture, brand and competitive stance.

Focus: Apple Intelligence.

State of the Union

Products & Services: Financial performance and market overview

Valuation: Measuring customer creation and retention

Growth: Opportunities in Products, Services, and Geographies

Externalities

Legal and Regulatory Review

Competition

Macro

China

Big Picture: Adoption Rates, Sustaining and Disruptive roadmaps

Wild Card: Reading the Buffett portfolio decision

We’re maintaining the intimate atmosphere of last year: same venue in Boston and limited in-person seating allowing for seamless interaction and enquiry. In addition, we would like to address a wider, global audience. So, for the first time, we will also be offering remote participation where you can watch the livestream, ask questions, and discuss topics live.

Tickets are available now. Asymco followers can get an additional discount using code asc24.

The Apple Vision Pro has had a very long gestation period. The first evidence for it emerged in 2015 when Apple acquired Metaio and Mike Rockwell was hired. That’s almost 9 years ago. Even at this time, the product is in many ways incomplete and will take some years to develop into its potential.

So why is this taking so long? How does it differ, it at all, from other product developments at Apple? And what was the decision process for the product? Was it different than other Apple products? Now that we have the product to use, it’s possible to hypothesize answers to these questions and examine how Apple is evolving in its own long-term trajectory.

After using the product for a few weeks my observation is that the development of the Vision Pro appears to have been an engineering-led heavy lift rather than a design-led puzzle solving. To suggest such a distinction between engineering and design is perhaps obvious but it’s not so obvious for Apple. Historically the two disciplines were blended imperceptibly or forged into a whole by management. Not without difficulty but forged nonetheless. I therefore think that this effort is a departure.

For the Vision Pro there were significant measurable performance requirements such as resolution, frame rates, tracking (eye and hand) accuracy, response times, weight/size, and power consumption which all needed huge leaps forward. Orders of magnitude. None of these were good enough for those nine years and some are still not good enough, especially for mass adoption. This is before considering the software and ecosystem which need to be built for an entirely new experience. All of these breakthroughs are against hard physical (biological) constraints. Engineering is all about balancing physical constraints, making tradeoff decisions in pursuit of some optimum. The Vision Pro was hard to develop because it requires all these inter-related constraints to be balanced.

In contrast, design decision making has to consider purpose. It leads to more of the human and environmental (economic) factors: what is the user trying to do? What are the limitations of the person using it and what are the circumstances of the usage? What should be the goal? It’s more a question of why than how. Design is answering the Job-to-be-done question whereas engineering is answering the how-to-get-it-done question. Apple’s leadership in product over the years was due to their insight into both of these questions. As Jony Ive would say: saying no to a thousand good ideas and focusing only on what mattered, based on keen insight into the human condition. Another way of saying that a product needs to justify its existence.

Design is not just how a product looks or feels. It’s how the user discovers it and thus why it exists.

The purpose of the Vision Pro is however all too brief: to enable a new human/computer interface. The very premise that created Apple: make computers easier to use and thus make them more useful and more used. The developments of silicon and optics and batteries and communications of the last few decades have suggested that there was a leap possible beyond the prevailing touch interface. Multitouch itself was a leap from the trackpad/mouse which was a leap from the keyboard input method. All these leaps cause Apple to surge forward, delivering a sequence of futures in a way that made them absorbable by many if not most.

In addition, the Vision Pro is not a product that the user needs to look at while using it. It’s completely invisible, having no physical presence to the user. You look through it rather than at it.

Therefore there is no question of “Why” or “How to use it”. These are self-evident. Consider the user’s input. The interface of looking at something and touching fingers together is so direct that there is no need to learn it. You rather need to unlearn the “computer” interface to use it.

Now consider the output: The canvas to paint on is not a rectangular screen with rounded corners and perhaps a pill-shaped cutout. It’s the entire world. It’s all that you can see. It’s not in front of you. It’s all around you. The place you use it is not in your hand, on a desk or a slice of time. It’s anywhere and anytime. In other words, we don’t need to have–as there was with the phone–“a conversation” with the user to discover what is missing and what can be fixed. If anything, the design surface is everything and everywhere.

The premise of spatial computing is that computing is consciousness itself. All that you see, everywhere you are, with no friction of “interaction” or “input/output”. There is no “user interface”. There is only space, natural and synthetic.

So it follows that this product is different. The Vision Pro is a project to develop not just a new computer but a new way that computers are used.

Before going into how exactly, let’s recall that when the phone was made mobile it made calling a person possible. Before the mobile phone, calling meant calling a place. To call a person meant guessing where they would be. Going to calling a person, and not just a place, meant all people were callable and also all people could be callers. Once data was provisioned to the phone then all people could not only consume but they could also publish. Anything and always. Which they did, for good and bad.

The Apple Vision Pro is aiming to do even more. It’s saying that computing is not something you initiate and terminate. Or that you do in a place. With a phone you stop, look, act and then go back to what you were doing before. Spatial Computing is ambient. It’s wearable. The Apple Watch is also an ambient computer but it has limited output. It’s so limited that it’s essentially consumed with a single glance. The Vision Pro is the opposite. Every photon you see, it generates. To avoid it, you close your eyes.

For this reason, the classical questions of design are moot, or at least they are moot on the device. They become relevant at the app layer. The device is bionic. It’s defined by biology not consciousness. The questions of what to paint on the canvas the user sees, i.e. the world, is left as an exercise to the developer.

The product strategy, go-to-market and all the details we are witnessing related to launch and packaging are a byproduct of this essential distinction. The development process, the ecosystem questions, the price points. They are all what they are because this is such a giant leap forward. It must be understood for its profundity and that will not be quick or easy. It’s unintuitive really. Rather like Special Relativity was when Einstein proposed it. It is still unintuitive today because it makes sense only on cosmic scales (and the speed of light.)

So I propose that those who might want to consider this new spatial computing era should call it something else: spacetime. The time spent in spatial computing but also this new era we are entering.