The International Federation of the Phonographic Industry (IFPI) reported that global digital revenues were $5.6 billion in 2012. This represented about 9% growth from 2011 and accounted for 34% of total industry revenues[1].

Apple regularly reports iTunes as a separate revenue item and occasionally it also reports payments data for developers and app download rates. By interpolating the data published and combining it with some assumptions it’s possible to estimate the mix of revenues (and costs) associated with iTunes.

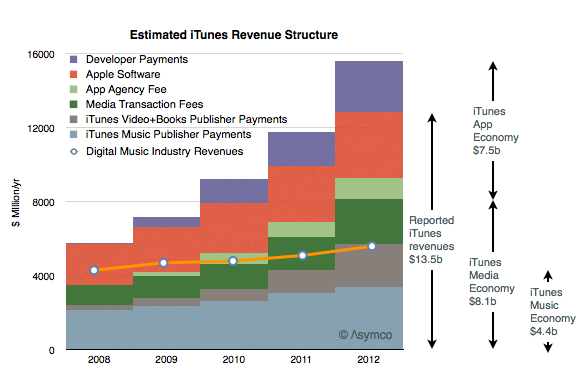

My yearly estimates are summarized below.

Note that I also included historic digital music industry revenues (as a line). I also included the following summary items:

- iTunes reported revenues were $13.5 billion (including Apple’s own software sales)

- iTunes gross revenues were about $15.6 billion (including payments to developers)

- The iOS and OSX “App Economy” was about $7.5 billion while the iTunes “Media Economy” was about $8.1 billion (both figures include transaction costs.)

- The iTunes Music economy was $4.3 billion of which $3.4b was paid to music labels.[2]

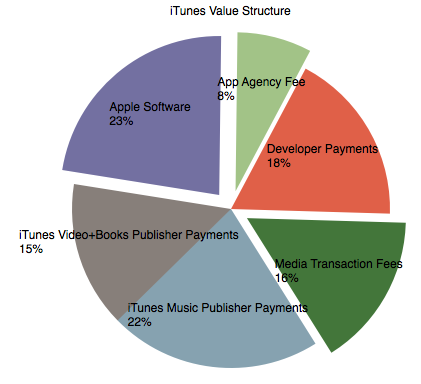

In terms of percent of total value the components are:

Looking at growth, these estimates imply that App revenues are growing at about 50% while iTunes Music is at 10% and Video+other at 90%.

Looking at profitability, there is potential for operating margin in Apple Software and App Agency Fees and perhaps some of the Media Transaction Fees (exploded wedges above). Historically, Apple suggested that their App and Media stores ran at break-even but that may no longer be the case. Operating margins from Software may be significant.

—

Notes:

- These revenues were from recorded music and don’t include live performance

- My estimate for the iTunes Music payments to publishers is equivalent to about 60% of total industry revenues.

Discover more from Asymco

Subscribe to get the latest posts sent to your email.