Apple will generate 2X as much handset profit as the rest of the industry combined this year DESPITE SELLING ONLY 3% OF THE HANDSETS BY UNIT VOLUME

via You Can’t Appreciate How Completely Apple Has Humiliated The Cellphone Industry Until You See These Charts.

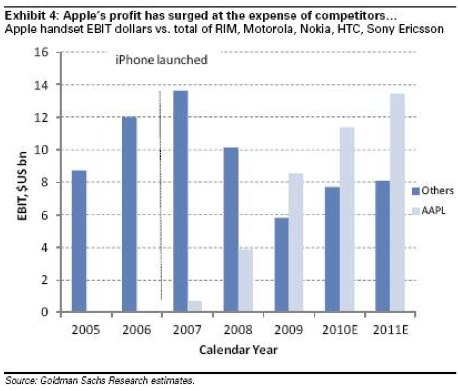

That interpretation of the data is exaggerated and/or incorrect. An analysis of profitability was done with respect to Nokia here and industry-wide here.

Goldman Sachs analysis (graph below) shows competitors’ profits and losses combined. Sony Ericsson and Motorola generated negative profits during 2008 and 2009 and may do so through 2010. Apple’s profits are likely to be larger than the industry *net* profits but not twice as much by 2011 (the graph does not even show that; 13.5 is not twice 8). Furthermore, the competitors do not include Samsung and LG!

Exaggeration or not, the fact remains that Apple entered the market in 2007 and in only three years became the most profitable phone vendor. It’s indicative of the value of an integrated user experience innovation in the market, which itself is indicative of the value of software in a hardware-oriented incumbency.