We reflect on why the narrative on Apple has changed post-WWDC and analyze both the evolution and consistency of Apple’s culture. Furthermore, what elements of that culture/process/priority setting can be copied? In other words, what does it take to be great?

Late late majority

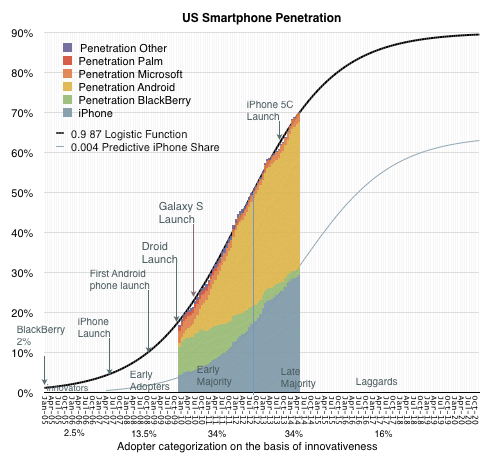

Seven years after the iPhone was launched, 70% of the US population is using smartphones. Smartphones existed before the iPhone so the category is older than seven years but as far as adoption goes this is nearly the fastest ever.

The CD Player reached 55% in seven years and the Boom Box about 62%. If measuring the period between 9% penetration and 90%1 the smartphone in the US will have a lifespan of about 9 years starting in 2008. Before this period, the product was largely experimental and participating vendors2 mostly failed. After this period most products will be “commoditized” with decreasing margins and increasing consolidation.

The rapidity of growth is all the more remarkable given the penetration is at the individual, not household level. The total user base is therefore over 270 million rather than the 115 million usually targeted by consumer technology, nearly 60% more purchases. This is also remarkable because the product has a shorter lifespan of use (two years) than is typical for other consumer technology products3

We are therefore now in the “Late Majority” phase of the US market. This is not a surprise. The inflection point in the market occurred in mid 2012 so we’ve been in this phase for two years already. It’s not therefore controversial to predict two years of continuing though decelerating growth.

As Geoffrey Moore explained, the marketing of technology products needs to be varied as we get into different phases of the market. Innovators (first 2.5%) need to be sold on the premise of novelty itself. Early adopters (next 13.5%) seek status and exclusivity. Early majority (34%) seek acceptance and Late Majority (34%) seek pragmatic productivity. Laggards (last 16%) seek safety.

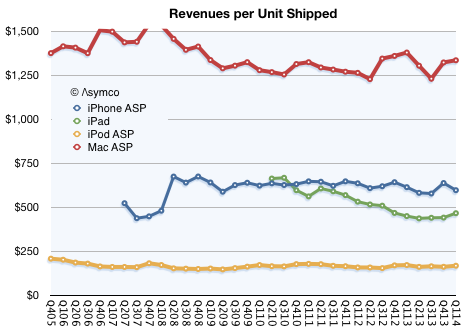

One aspect of this adoption cycle that is misunderstood is the role of pricing. The assumption is that pricing matters more as adoption increases. This is misunderstood because pricing always matters and therefore it never matters. Pricing is one of many elements of marketing mix and at any time there are product choices across a wide spectrum of pricing. Pricing is also a signal which can be elaborately obfuscated through bundling and unbundling.

One way to illustrate this is to consider how Apple products behave in the late phases of markets. Apple products have notoriously firm pricing.

The revenue per unit of Macs, iPods, iPhones and iPads remains stubbornly consistent. This is not to say that each unit sold is the same price. The company tweaks “the mix” of mid, low and high products to keep the average selling price constant. But fundamentally the average remains constant which means that regardless of market phase, Apple retains its margins.

So as we look forward to the last two years of growth for smartphones, how will Apple fare? Continue reading “Late late majority”

Competing effectively against your most potent competitor

New market disruptions take root in non-consuming contexts. For instance, mobile phone photography began not because early phone cameras were good. They weren’t good at all but good enough when a camera was not within reach. The quality was poor but the photo taken would not have otherwise been taken, making a lousy photo better than no photo.

The result is that the total number of photos taken this year will be ten times higher than the total number of photos taken before the advent of mobile phone cameras.1

This rush to use the phone as a camera has meant that phone makers are keen to improve their product (so as to compete effectively with it against each other) and as a consequence they overtake the incumbent camera makers in quality as well as quantity.

The same phenomenon was experienced by fixed component “Hi-Fi” audio products. The quality of mobile music was poor but it was convenient and convenience translated into consumption and consumption translated into quality improvement and eventually the evaporation of usage of the traditional category.

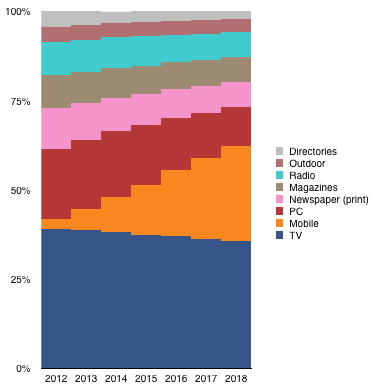

Now consider how ad dollars are getting spent. The following chart shows the eMarketer forecast for ad spending mix across different media in the US.

It would appear that the “Mobile” media is competing effectively against the other media types, especially the non-Mobile digital (i.e. PC-based experiences).

However, if we look at the absolute spending forecast the picture shows that Mobile is responsible for most of the growth in the overall spending. Continue reading “Competing effectively against your most potent competitor”

- The total number of photos taken in 2014 is likely to be around 880 billion. Prior to 2000 the total number of photos ever taken is estimated at 85 billion. [↩]

Apple: Lessons in Self-Destruction. Richard Gutjahr’s blog

My thanks to Richard Gutjahr for taking time to talk about self-disruption. I met Richard as the Master of Ceremonies at the Censhare FutureDays event in Munich. He interviewed me for his blog and posted the results as a video and sound file. Richard is a journalist (Berliner Tagesspiegel, Frankfurter Allgemeine Zeitung) and TV personality (news presenter for Rundschau night).

Horace and I have met at a conference in Germany a few weeks ago. During a break, we were talking about the future of Apple. Horace made a statement, which I found quite intriguing: In order to remain innovative, it is not enough to reinvent yourself again and again. Apple must be the one to destroy its own business.

Hour-long conversation including audio and video: Apple: Lessons in Self-Destruction.

The Disruption FAQ

Q1. What is disruption?

Disruption happens when the strong are defeated by the weak. More precisely it’s when those with unconstrained access to resources have them taken away by those with minimal or no resources. It’s a phenomenon that is in contrast to sustaining competition where the strong get stronger.

Q2. How can disruption happen? Don’t the strong always have an advantage over the weak?

The strong can be defeated when the fight is unfair. More precisely, “strength” is only a perception based on convention or historic precedent. The entrant may be weak in resources but may be strong in a way that is not seen as conventionally useful or valuable such as agility or a willingness to learn.

Q3. What makes a fight unfair?

A fight is unfair if the opponents fight according to different rules. This is also called asymmetric competition. Asymmetry is an important concept in game theory, economics and military science.

Q4: Is there a way to know disruption is about to happen?

Disruption theory is an attempt to reliably identify winning challenges. It includes a method of analysis of “the setting” of the fight and “the weighing” of the fighters. In other words, it measures whether the challenger is sufficiently asymmetric and whether the incumbent is flexible enough in their likely response. If there is insufficient asymmetry the theory would suggest the challenger will lose, and vice versa.

Q5: How often does it happen?

In some industries it happens quickly and in some industries slowly and in some never at all. Determining the cause of the rate of disruption is an important research topic. We can hypothesize that industries which show frequent disruption also show a high degree of wealth creation. The inverse is also true: industries that don’t get disrupted don’t create much wealth.

Q6. How do incumbents react to asymmetric challenges?

This quote (mistakenly attributed to Gandhi) describes it best: “First they ignore you, then they laugh at you, then they fight you, then you win.” The main test of asymmetry is to ask whether a challenger’s entry is ignored (or welcomed) by the incumbents. Most asymmetric challenges are not taken seriously because they initially benefit the incumbent. The side-effect is that it lulls them into a sense of security resulting in a lack of response. Challengers have the child-like advantage of rapid growth and learning while incumbents are encumbered by their size and lack of flexibility.

Q7: Why don’t challengers respond in kind?

Mainly because they don’t feel that they need to. The newcomer is either not seen as a threat or welcomed because the customers they obtain that are not seen as valuable. In some cases the business model of the entrant is contrary to that of the incumbent. In other words, the challenger makes money in a way that would cause the incumbent to lose money. Often the challenger is actually invisible because she misdirects attention. They may be seen as competing in one market with a certain set of competitors but their effect is in another market which never had to deal with a challenger.

Q8: If there are different ways disruption can be observed, doesn’t that mean there are different types of disruptions?

Yes. When a competitor challenges with a cheaper product that seems to perform poorly and has low margins and the incumbent accepts the entry because it allows them to concentrate on more profitable customers then this is called a “low-end disruption”. Here the asymmetry is in cost structure. The entrant has lower costs and accepts lower profit margins and may “make money” in new or different ways.

When a competitor misdirects attention by selling a product that draws usage from existing customers and adds non-consuming new customers because it enables new uses, then the incumbent feels no pain from the entry because they don’t sense a reduction in customers. We call this a “new market disruption“. The challenger gains a foothold and grows/evolves, eventually capturing customers exclusively. Here the asymmetry is in the basis of competition and measurement of “performance”. The new product does not actually do the same thing as the incumbent product or does a subset of valuable tasks poorly while excelling at menial tasks. The entrant may be highly profitable but they are not taking profits away from incumbents because they “grow the pie”, capturing value by fulfilling unmet needs.

Disruption can also happen to professions and institutions when less skilled individuals are enabled to perform complex jobs or when professionals can establish good enough services that used to take institutional support. This is called professional services disruption.

Technological change is often (but not always) the core enabler in creating disruptions. The analogy is that technology is a weapon that allows asymmetric combat but the combatant is the disruptor, not the weapon1.

Q9: It sounds like the trick to spotting disruption is in perceiving when the fight becomes “unfair” and an outsider advantage is gained. Does the theory make this easy?

It makes it possible but not easy. Understanding when a basis of competition changes and where competition is shifting is still very difficult. It is notoriously difficult to sense when it’s happening to you because you are working toward a strategy with assumptions that have been tested and proven to be correct. In other words, you, your colleagues, your competitors and everyone you’ve ever met knows the rules of the fight. Insider status makes you an expert, your knowledge is far beyond a lay person’s and you have a track record of winning. Hubris and pride makes it difficult to accept a challenge from an ignorant outsider.

Furthermore, an outside analyst who is not suffering from these psychological weaknesses may not have the means to measure change because they don’t have access to market metrics. So you can’t typically hire a consultant to help you spot it. This is where the theory helps. If you are a practitioner then you can use the theory as a lens to see the patterns in the operating data.

The proper application of the theory requires domain knowledge or deep reading of weak signals. It’s best employed by incumbent operating managers analyzing their own industry. It’s a tool that can be used to overcome the perception of incumbent invulnerability. It is not a tool that can be used by armchair generals. They can pick up the lens but, not having any data to look at, they have have no patterns to recognize. (This last point is disputed. See comment.)

By the way, entrants don’t benefit much from it either because they act disruptively by instinct. They enjoy the freedom of having nothing to lose.

Q10: How long does this take? Isn’t a shift in competition natural over a few decades?

The speed of disruption is changing rapidly. It used to take decades but now it takes years and in some software industries it could be happening in less than one year. When it used to take decades it did not matter much because the “victims” of a disruption usually could spend a career in the firm being disrupted and would not have to adjust their behavior or assumptions. The consequences would have been felt by future generations. The rate of disruption today is so rapid that many careers and lives and families are having to deal with the consequences, sometimes more than once. Estimating the acceleration and scope of disruptive change is a great research topic.

Q11: Is the theory complete? Can’t we just write an app for it?

It’s not complete. It cannot be encoded as a deterministic algorithm. It’s not even likely that expert systems or neural networks or machine learning can help. This is because perception of change in competition is a skill informed as much by intuition as by data and rules. If the theory is developed further, through a process of theory building, then it might become an app.

Q12: If the theory is not complete, then isn’t it useless?

A theory is not useless if it’s imprecise or difficult to use. Data that would make conclusions precise is often missing or unavailable. The theory relies on weak signals and explains what used to be unexplainable. Many sciences developed from empirical analysis similar to where we are with disruption theory. Theories benefit from development.

Q13: Is the theory being developed further?

Yes. There is a process for theory building which has been ongoing for over a decade where many researchers, students of disruption and practitioners are contributing.

Q14: Can the theory be applied outside of business competition?

Yes, institutions can be disrupted as can individuals. Possibly even economies and states. This is because a growing technological base and communications enable asymmetries of ever-greater scope and speed. The research needed to establish how this happens is under way. However it’s important to know the limits of the phenomenon. Incumbents are getting wiser as they wield the theory and some “settings” show resistance to change and thus prohibit technological cores to be utilized disruptively. The study of these anomalies is essential to the process of theory building.

Q15: Is disruption a force of nature? Has it always existed? Will it never end?

Oral traditions suggest that people have been aware of disruptive forces for all of history. We feel it in the school playground and in many personal relationships. It’s in the Bible and the classics that predate it. It’s visible in all cultures. Disruption theory as applied to business and government is only an extension of this causal individual behavior into complex systems. It’s possible that awareness of it might cause the behavior to change, or, put another way, that if you observe and understand the phenomenon, that knowledge could cause it to stop happening. But the systems involved are vast and learning curves are long. Enlightenment may take a few lifespans.

Update:

Here are questions which have been added based on reader feedback. Please feel free to suggest others in the comments.

Q16: Isn’t Disruption just evolution of business models?

Business models evolve, but if the evolution sustains an existing incumbent then it’s not a disruption. If an evolution is adopted by an entrant who then proceeds to strip the assets and profits from an incumbent then it’s a disruptive change. The key question is why do some changes get adopted and not others.

Q18: What have been the major improvements in the theory since its introduction in 1997’s The Innovator’s Dilemma?

From Clay Christensen’s work alone: New Market Disruptions, Professional Disruption, Value Chain Evolution Theory, Jobs to be Done Theory. The Innovator’s Solution including how to respond with autonomous self-disruption, the role of acquisitions, the study of Healthcare and Education as targets of (and anomalies to) disruptive change. The process of theory building. The Capitalist’s Dilemma and how economies create incentives and disincentives to disruptive innovations. Many other contributions from researchers too numerous to cite here.

Q19: What industries cannot be disrupted

Industries which experience no disruptions are “anomalous” in that the theory suggests that technological progress forces change and technologies have proliferated in almost all industries.. Industries or institutions which have remained largely undisrupted include Energy, Education, Government, Healthcare, Airlines and Hotels. The study of these anomalies continues and explanations identify conditions that prevent growth. Dependencies on regulation, infrastructure, and absence of technological core enablers caused some of the atrophy to date. However signals of change are appearing in all these industries and paths to disruption are clearly possible.

Q20: How is it possible that companies which were claimed to be disrupted are still around and some which are claimed to be disruptors have vanished?

Being disrupted does not mean ceasing to exist. Being disrupted is a loss of a specific encounter, but not necessarily a terminal loss. Being a disruptor is a win in a specific encounter and not a guarantee of immortality. Indeed many disruptors come to be disrupted and the theory suggests sustainable growth requires self-disruption. Also a disrupted company can be re-configured post-disruption into another entity or can muddle along with limited value indefinitely. Sometimes they can rise up and become disruptors again.

- See David vs. Goliath: using a projectile allowed David to overcome Goliath but only when wielded skillfully [↩]

Ten years ago: Clayton Christensen on Capturing the Upside

You can hear this as an MP3.

[It’s important to understand just how much the theory has evolved in the last 10 years. Much more perhaps than in its first eight.]

Doug Kaye: Hello, and welcome to IT Conversations, a series of interviews recording and transcripts on the hot topics of information technology. I am your host, Doug Kaye, and in today’s program, I am pleased to bring you this special presentation from the Open Source Business Conference held in San Francisco on March 16 and 17, 2004.

Mike Dutton: My name is Mike Dutton, and it is my pleasure to introduce to you today Clayton Christensen. Professor Christensen hardly needs an introduction. His first bestseller, “The Innovator’s Dilemma,” has sold over half a million copies and has added the terms “disruptive innovation” to our corporate lexicon. His sequel — and you have to have a sequel to be a management guru — is entitled “The Innovator’s Solution” and is currently Business Week’s bestseller’s list. Professor Christensen began his career at the Boston Consulting Group and served as a White House fellow in the Reagan administration. In 1984, he cofounded and served as chairman of Ceramics Process Systems Cooperation. Then, as he was approaching his 40th birthday, he took the logical step of quitting his job and going back to school, where he earned a doctorate in Business Administration from Harvard Business School. So, today he is a professor of Business Administration at Harvard Business School where teaches and researches technology commercialization innovation. Professor Christensen is also a practicing entrepreneur. In 2000 he founded Innosight, a consulting firm focused on helping firms set their innovative strategies. And according to a recent article in Newsweek, “Innosight’s phones ring off the hook, and the firm cannot handle all the demand,” very similar to all the startups in open source here today. So, please join me in welcoming Clayton Christensen.

Clayton Christensen: Thank you, Mike! I’m 6 feet 8, so if it’s okay, I’ll just…the mic picks up okay. I’m sure delighted to be with you, especially because there is blizzard in Boston today; my kids have to shovel the snow!

As Mike mentioned, I came in to academia late in life, and the first chunk of research that I was engaged in was trying to understand what it is that could kill a successful, well — run company. And those of you who are familiar with it, probably know that the odd conclusion that I got of that was that it was actually good management that kills these companies. And subsequent then to the publishing of the book that summarized that work, “The Innovator’s Dilemma,” I’ve been trying to understand the flip side of that, which is if I want to start a new business that has the potential to kill a successful, well — run competitor, how would I do it? And that’s what we tried summarize in the book, “The Innovator’s solution.” It’s really quite a different book than the “Dilemma” was, because the “Dilemma” built a theory of what is it that caused these companies to fail. And then in the writing of this solution, I’ll just give you analogy for where we came out on how to successfully start new growth businesses.

I remember when I first got out of business school and had my first job. I was taught the methods of total quality management as they existed in the 1970’s, and we had this tool that was called a “statistical process control chart.” (Do they still teach that around here?) Basically you made a piece, you measured the critical performance parameter and you plotted it on this chart, and there was a target parameter that you were always trying to make the piece to hit, but you had this pesky scatter around that target. And I remember being taught at the time that the reason for the scatter is that there is just intrinsic variability and unpredictability in manufacturing processes.

So, the methods that were taught about manufacturing quality control in the ‘70’s were all oriented to helping you figure out how to deal with that randomness. And then the quality movement came of age, and what they taught us is, “No, there’s not randomness in manufacturing processes.” Every time you got a result that was bad, it actually had a cause, but it just appeared to be random because you didn’t know what caused it. And so the quality movement then gave us tools to understand what are all the different variables that can affect the consistency of output in a manufacturing operation. And once we could understand what those variables were and then develop methods to control them, manufacturing became not a random process, but something that was highly predictable and controllable.

Continue reading “Ten years ago: Clayton Christensen on Capturing the Upside”

▶ Horace Dediu: “Transformation of Business and Society through Technology”

My talk on the future of things from Censhare’s FutureDay 2014 in Munich.

Asymcar 15: Sunray Sedan

Matt Grantham joins us to discuss electric vehicles, renewable energy, smarter software, solar opportunities and economics. Matt introduces us to Solar X, the solar car challenge. He reflects on these emerging technologies in light of Australia’s nearly extinct auto manufacturing sector.

We explore the concept of a car as the home power source and consider possible EV disruption of traditional power generation and distribution concerns. The potential business models arising from these emerging technologies makes us pause in light of solar firm’s stock performance.

Twenty Questions from Catalin Stelian Andrei

Catalin Stelian Andrei, Editor of The Day, INTERNET PROTV asked me twenty questions:

1. What phone do you have in your pocket right now? Why that model?

I carry the iPhone 5. The last iPhone I bought was an iPhone 5C which I gave to a family member.

2. Apple is going to launch, form all we know, an iPhone with a bigger screen, long after their market rivals. Is Apple one step behind, being forced to take this road in the fight with Android and Windows Phone devices? Because many smartphone users were hoping that an big screen iPhone, a redesigned model, will be lauched long time ago, and that didn’t happen.

Making bigger phones is easier than making smaller phones. First because miniaturization has always been the most difficult engineering challenge, and second, because a smaller phone has a smaller battery making efficiency much more important. The larger the phone, the simpler it is. The third reason smaller is more valuable is that it’s easier to carry and use. The largest phones cannot be put in pockets and cannot be used with one hand. In the history of consumer, electronics size reduction has been the most consistent measure of performance, and the most rewarding. Usually the most exceptional reductions in dimensions create the highest price and profit bands. There have been niches for larger portable devices but they are consistently a small part of the overall market. If Apple were to introduce a larger device I hope they will be able to solve usability problems and make the category attractive to a larger audience.

3. What do you expect from the new iPhone 6?

I expect it to run the latest version of iOS and, with the new apps developers will ship, that should make the most impact in people’s lives. I imagine health maintenance and home automation will become valuable new franchises. Of course iOS 8 will also run on older iPhones, but I suspect the newest iPhone will somehow run the new software better and have smoother integration with services.

4. What’s the “not to do” lesson that Apple needs to learn for the now iPhone from it’s own past experience or their competitors?

The biggest challenge is to move rapidly with scale. The company has managed to grow from zero phones a year to hundreds of millions. That’s great but it’s still frustrating to wait one year for major improvements. The “cycle time” of innovation for Apple remains one year. I wish it could be faster but perhaps this is also too fast for some. In some services like maps and iCloud and iWork, which are independent of hardware (mostly,) speed is of the essence.

5. The iPhone is the most expensive smartphone on the market right now. In Romania, it certainly is. But where does Apple gains it’s most money from, selling products to users or selling services, like iTunes, App Store? And having that in mind, what will be their next step: better – breakthrough products or bigger, more complete services?

The answer to where a company “gets its profits” is best answered by asking where a buyer “gets his value” from the product. For instance you might answer the question of where a car company gets its value by saying that it’s from making people be in more than one place in a day. So the “differentiation” of a car is in answering the question slightly differently. If it’s hard to see a difference to this answer between cars then it’s hard for any one company to make a profit. For a company like Apple, we need to ask what its users value about the experience and why they are willing to pay for that. My hypothesis is that the brand’s value is in making life a little bit easier. That’s what Apple competes on. Of course, some people are not willing to pay to have an easier life and some even want to make their lives more complicated so Apple’s proposal to make life easier, for a price, is not accepted by everybody—which is ok by them. But for many, paying for comfort, productivity and ease of mind is worth quite a bit. The reason Apple is able to gain a premium over the competition is that this value proposal (of paying for simplification) is either weak or non-existent for competitors. Indeed, many competitors compete on the basis of making life more complicated.

6. What does innovation means for Apple right now? What are their options for assuring a next decade of success? A new Steve Jobs person or a Steve Jobs tipe of group thinking. How hard is that to achieve?

Innovation is meaningful invention—bringing useful creations to a large number of people who then make use of that creation. The interesting aspect of making money from innovation is that it’s a rare phenomenon, requiring many disciplines to work together. It’s like a big movie that somehow works and becomes widely popular but costs little to make. Many movies are made, few are successful and very few of those which are successful are built at low cost. What we know about technology innovation is that it’s a combination that comes together under strong leadership but that leadership alone is not sufficient. The myth of Steve Jobs is that he was both necessary and sufficient to success. The truth is that he was necessary but not sufficient. To make successful innovations requires strong leadership and teamwork and a process of incentives and passion that is hard to create a formula for. How this works at Apple is its biggest secret.

7. Who are the key Apple employees right now? Do they need another Jobs or do they already have him?

All Apple employees are key. I would say that’s the magic formula. There is no chief magical officer (and there never was.)

8. What will be the next best thing for Apple? […]

I don’t know. It’s probably not knowable. Continue reading “Twenty Questions from Catalin Stelian Andrei”

Asymcar 14: Grand Prix. An interview with Ossi Oikarinen

An interview with Ossi Oikarinen, Technical Director at Team Rosberg, a 30-year veteran of motorsport, Formula One TV presenter and deep insider.

We cover Grand Prix racing and DTM touring cars from the point of view of business models, jobs to be done and technical innovations. We touch on many other fine points.

This is a good one.

via Asymcar 14: Grand Prix. An interview with Ossi Oikarinen | Asymcar.